Creating your stream of guaranteed retirement income

Creating Your Stream of Guaranteed

Retirement Income Infographic

A retirement resource for individuals and couples

[Graphic of Guardian logo]

Creating your stream of guaranteed retirement income.

Your life doesn’t stop when your career does. The one thing you don’t want to stop, is your paycheck. [Photo of a man paddleboarding on a lake]

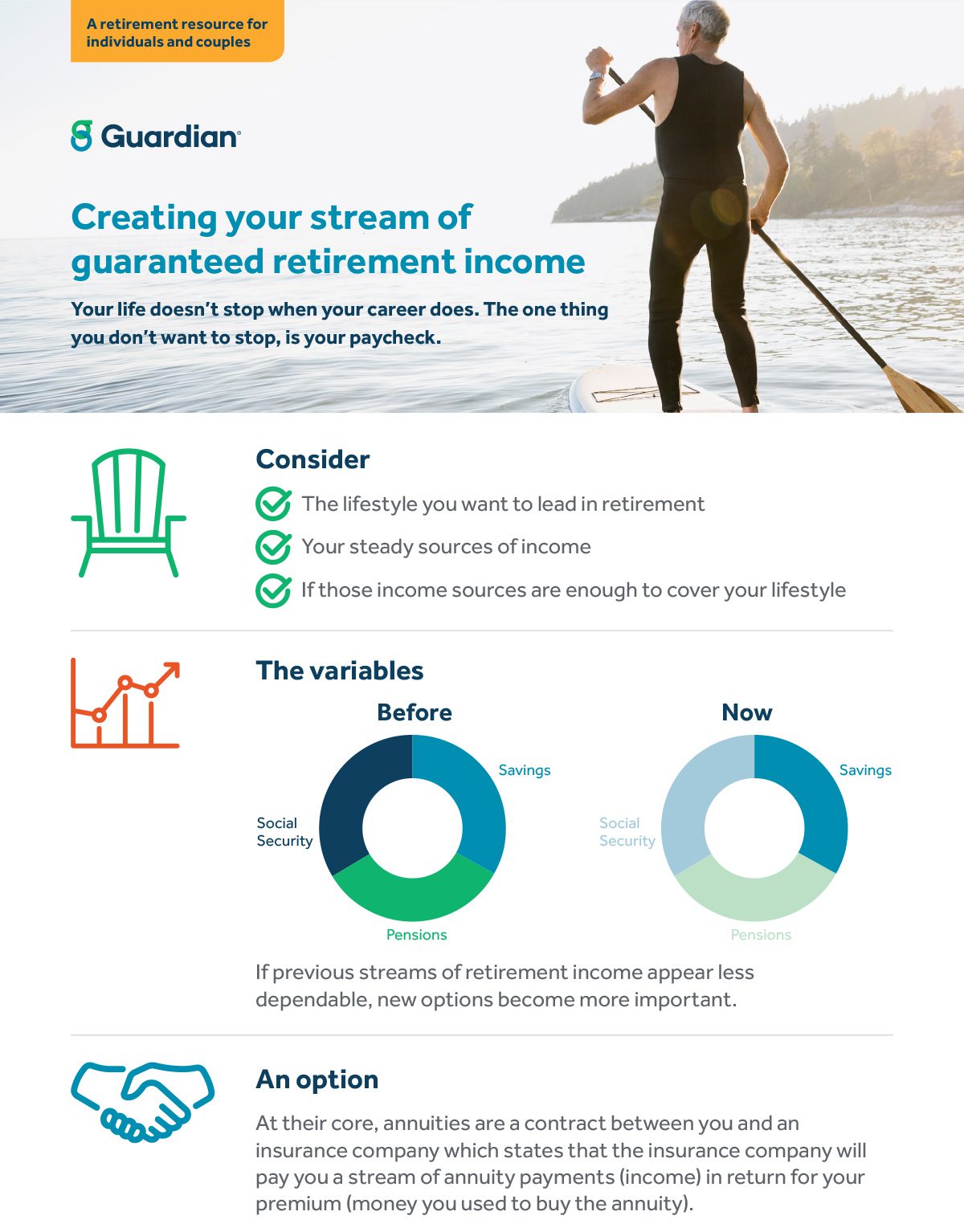

[Graphic of an Adirondack chair] Consider:

- The lifestyle you want to lead in retirement

- Your steady sources of income

- If those income sources are enough to cover your lifestyle

[Graphic of a line chart trending upward] The variables:

- Before [Circle chart displaying Savings, Social Security, and Pensions evenly distributed]

- Now [Circle chart showing Savings, Social Security, and Pensions, with Social Security and Pensions faded]

If previous streams of retirement income appear less dependable, new options become more important.

[Graphic of two hands clasped in a handshake] An option:

At their core, annuities are a contract between you and an insurance company which states that the insurance company will pay you a stream of annuity payments (income) in return for your premium (money you used to buy the annuity).

[Graphic of a play out of a playbook] How it works:

When the income stream starts depends on the type of annuity that you purchase.

[Circular graphic of insurance company in the middle with someone paying the premium at the start of the cycle and “immediate” as the other part of the cycle, ending in annuity payments] Single Premium Immediate Annuity (SPIA):

Pay a premium up front to receive income payments immediately. Consider if:

- You want immediate payments

- You want a guaranteed, steady income stream through retirement

[Circular graphic of insurance company in the middle with someone paying the premium at the start of the cycle with “deferral period” faded out as the other part of the cycle, ending in annuity payments] Deferred Income Annuity (DIA):

Pay a premium up front to receive income payments later. You can add

additional premium payments as well. Consider if:

- You want to secure income payments for the future

- You’d like the ability to add to your future income stream through additional premium payments

- You want to create lifetime income and help manage longevity risk

[Graphic of one small stack of coins and one large stack of coins with a dollar sign over the small stack] Qualifying Longevity Annuity Contract (QLAC)

A DIA that is issued in connection with a traditional IRA. A QLAC pays a lifetime income benefit that starts no later than the first day of the month following the owner’s 85th birthday. With the QLAC:

- You can defer paying taxes on a portion of your IRA assets for up to 13 years beyond what was previously allowed.

- You can have guaranteed income that you cannot outlive.

For more information please go to livingconfidently.com/myretirementreality.

The Guardian Insurance & Annuity Company, Inc. (GIAC), a Delaware corporation whose principal place of business is 10 Hudson Yards, New York, NY 10001 (800) 221-3253. GIAC is a wholly owned subsidiary of The Guardian Life Insurance Company of America.

Product availability and features may vary by state.

Annuity guarantees are backed exclusively by the strength and claims-paying ability of The Guardian Insurance & Annuity Company, Inc. (GIAC).

Guardian® is a registered trademark of The Guardian Life Insurance Company of America.

© Copyright 2022 The Guardian Life Insurance Company of America

The Guardian Life Insurance Company of America guardianlife.com New York, NY EB018014 (06/22) 2020-139866 (Exp. 06/24)

Living Confidently is powered by The Guardian Network.